|

|

|

To find out your Discount Rates, select the above button that best describes your business |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

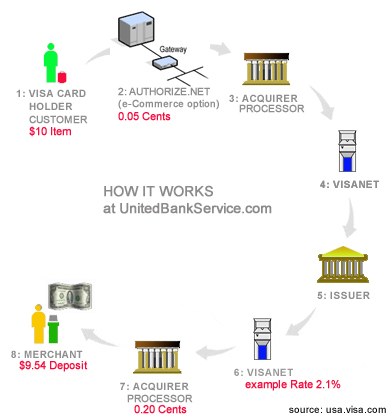

How does a business / merchant accept

credit cards? Step 1:

Your business (also known as the Merchant's Business) submits a credit card

transaction to the Payment Gateway (example Authorize.Net) when a customer

buys with a card, using your website or you process a payment with a Web Virtual Terminal

or a Retail

Terminal Swipe or by phone for MOTO Center or

with a

Wireless PDA Device.

Step 2: For Internet transactions, Authorize.Net receives the secured transaction information and passes it via a secured connection to us (Processor). For Retails terminals, transaction information are sent directly to us. Step 3: We submit the transaction to the Credit Card Interchange (a network of financial entities that communicate to manage the processing, clearing, and settlement of credit card transactions, such as VISANET). Step 4: The Credit Card Interchange VISANET routes the transaction to the customer’s Credit Card Issuer. Step 5: The Credit Card Issuer approves or declines the transaction based on the customer’s available funds and passes the transaction results, and if approved, the appropriate funds, back through the Credit Card Interchange. Step 6: The Credit Card Interchange relays the transaction results to us. Step 7: We store the transaction results for your statement and relay the results to you. Step 8: We pass the appropriate funds for the transaction to your bank, which then deposits funds into your personal Bank Account $$ within 24 hours. This communication process averages three seconds or less! |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Hassle free. Published Bank Rates updated

2019-10-23

* Hassle Free. Internet published Discount Rates are not available at our centers walk-in/phone-in, you have to apply online for these eSavings. If you are a retail and would like an Internet gateway, you will apply for both accounts. ::

Retails with an average $20,000 monthly sales can qualify for

0.30% Qualified Index Rate, by selecting SuperSaver on the online

application.

How is my merchant account supported? How can I make your day better? A very comprehensive support team is setup to assist you, consisting of 4 levels of operation. You will be provided with 3 toll-free numbers to reach supporting staff and subject experts.

How long will this offer last?

Our Solution:

All rates established here are long

term and guaranteed. This includes the cost of Authorize.net and POS

software which has not changed the last 11 years. We

make every attempt to pass the savings to you, however please

note that VISA/MC publishes the interchange rates twice a year

that all U.S. merchants are subjected to change; it may go down or up

or be regulated. All

standard merchant account discount rates

are Risk Free, as you have the ability to cancel at

anytime. You are also enrolled in one unique program

Join

the VIP Club for a guarantee low rate forever Join

the VIP Club for a guarantee low rate forever Our Invitation: Submit two recent processing statements of $100,000 in volume per month along with your online application for a guarantee life-time low rate. Select VIP Club on your application. When validated, we will send you a welcome VIP package which you will have 48 hours to complete the membership. [More Details] What fees are typically involved in accepting credit cards in the industry?. To better educate our clients, we always encourage our clients to compare, know the typical merchant banking fee structure and understand the terms offered by various banks and providers.

Recurring fixed monthly fees:

Monthly Gateway Fee (optional feature

only for Internet businesses) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Our Solution: UBS has a service agreement with Authorize.net to waive setup fees and provide a very low monthly fee. See rate table above. As a provider, our overall rates are much lower, you will be saving 10 cents or more for each transaction with no limits to the number of transactions. Authorize.net will support and bill you directly at the discount rate based on our service agreement. We also will provide you free scripts that allows you to create order forms on your web pages. read more about our integration solution. In addition, a free iPhone/iPad app for authorizing anywhere. If you are already tied to a merchant account, you can still select Gateway Only rates. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Monthly Minimum Processing Fee: The monthly minimum amount is

what you must pay each month for your Visa/MasterCard

processing, at the minimum. However, this fee is only billed when it is not

exceeded by your monthly processing fees. The monthly minimum

does not apply to statement fees or transaction fees. Our Solution: At UBS, we have WAIVED all monthly minimum with the exception if you opt to participate in our Free Terminal Program or Optional Offers. Waiving a monthly fee can easily save you money for new businesses. Keeping it just as attractive for established high volume businesses, we can waive your annual fee when you keep our low monthly minimum. To summarize, if your monthly minimum is $15, you will only need about $714 in VISA/MC sales each month. Apply online and select your choices. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

FSA HRA Do you accept Healthcare Spending cards mandated by the Federal government? Our Solution: Yes, as a Healthcare Merchant Provider, we accept Healthcare Provider Cards - Flexible Spending Account (FSA), Health Reimbursement Account (HRA) and Heath Saving Accounts (HSA). On your application, just request for these features during your terminal setup. Read more..

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Contractual Terms & Cancellation / Termination Fee

Our Solution:

There is NONE - $0 cancellation fee,

even though we would like you to stay for 3 months in good

faith. This is one of the key exit criteria that an

experienced merchant would want and should not be taken for

granted. We understand that it is a burden for some businesses

to be tied down financially, so we have negotiated a $0

cancellation fee for everyone with the exception for those who

customized a plan or

specifically requested for a term or on a Passport or have

purchased discounted equipment. The industry banking standard is 3

years, because there is a significant cost/risk to approve an account

for any single merchant. We review, audit and present your

business to underwriters; then your application will be sent to technical support, the billing department, shipping and

makes the final journey to

the filing station. You will quickly notice that this whole process requires the use of about

8 employees working behind the scenes to make it all

happen for you.

To Cancel:

A

simple process has been established for you. Before you

cancel, you may want to consider a no monthly minimum plan. To

cancel, call your assigned 800 number for a lesson on how to

close your books and how to handle refunds during this period if

your customer makes a request and plan how many days after your

last sale. Fax a signed letter to

authorize your cancellation. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Discount rates are always quoted

at Qualified Rate 1 in the industry and many banks/merchant resellers fail to inform

you about non-qualified rates. Each of your transactions will be

classified as either qualified, mid-qualified, or non-qualified.

These three classifications are based on Visa/MasterCard/Discover

rates, cost and risk management. Qualified (Ecommerce Rate 1) – This is your daily discount rate based on your merchant classification of MOTO or e-Commerce. Use a 3-D Secured Qualified Internet Ecommerce Gateway (example Authorize.net, QuickBooks) for Internet orders or Magnetic stripe is read and batch is settled within appropriate guidelines. Customers with standard issued card, check card, off-line debit, Corp Data III, Corp Data II Int’l, World Card Public Sector, processed directly through Authorize.net will have a Qualified rate.

Qualified (Card Present Rate 1) –

This is your daily discount rate based on your merchant classification of

retail, B2B, restaurants or office. To compete against PIN-based debit cards, Visa and MasterCard lowered the interchange rates for debit cards well below those for credit cards and pass on the lower cost of these cards directly to merchants. Cardholder and card must be present with a check card or off-line debit for Rate 1

and standard issued

card, Corp Data III, Corp Data II Int’l, World Card Public

Sector will have a Qualified Rate 2. Our Solution: Our principle has always been to provide low cost, value added services. The Qualified Rate 1 (also known as the discount rate) is the published lowest rate a merchant will incur based on the merchant classification each year and card used. The Mid-qualified is at a low range between +[0.00%..1.10%]+10 cents (e-Commerce at 0.00%) and Non-qualified surcharge is between +[1.30%..1.60%]+10 cents (e-Commerce at +1.39%..1.45%) spread above the Qualified rate. Rate charges are determined by VISA/MC at point of sale. With these surcharges, you can estimate your effective rate and will be pleased to discover how low our rates are. Your customer's decision on how they pay with their credit card is not within your control, you should therefore account for the cost as part of doing business with credit card payments. What VISA/MC/Discover have done, is to pass some of the risk and cost of promotion to you. As an added benefit, we therefore lowered your Qualified Rate upfront with a valuable base point discount, to give you a better effective rate.

Debit Card

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Tell me more about accepting credit card? A merchant account in the USA. is a contract under which an acquiring bank extends a line of credit to your business. As line of credit is money that has not been paid by your customers, it is very similar to you getting cash in advance deposited into your account within 48 hours after each sale. The underwriters will then accept the risks for 180 days, while your customers finance on their credit card. Your customer has not paid anything yet at the point of sale, so the money has to come from somewhere. A sponsoring VISA/MC Acquirer Bank or American Express will therefore underwrite your account and advance you the cash.

When you, as a Credit Card Merchant,

want to accept a credit card for payment of your goods and

services, you first submit an authorization transaction to your

Processor.

Along with accepting credit cards is

the responsibility of handling chargebacks and retrievals

[b3].

A chargeback is a transaction that is in dispute by the

cardholder or issuing bank. The chargeback occurs when a

customer disputes a charge or the bankcard procedures are not

followed. There are several reason codes for a chargeback

including merchant fraud, product/service not as described,

never received product/ service, transaction not authorized by

cardholder, etc. If you handle your sales properly and smartly,

you will not have any chargebacks at all. If

your business receives a chargeback, your checking account will

be debited for the amount in dispute. In addition, a fee for

handling the chargeback may be imposed and reflected on the

merchant statement. In some circumstances a cardholder’s

issuing bank may request a copy of the retail sales slip

containing the authorized signature. This is why it is essential

to keep accurate records of all sales slips and/or sales drafts.

Federal law requires merchants to maintain signed sales slips

for a minimum of two years and of course VISA/MC holds you

accountable for any customer chargeback up to 6 months. The

retrieval request will provide the cardholder’s account number,

a reference number. In support of the

You may be subjected to other standard inter-bank fees

[b3] if an incident occurs: Voice Authorization is used at times in a Retail store the old fashion way, when a card is in question. A merchant can call VISA/MC/AMEX directly for an authorization if your terminal indicates it or if you prefer to speak to an agent in person, typically for 60 cents. However eCommerce users should just use the virtual terminal- Authorize.net to obtain a card authorization, which cost you nothing additional. You will not use Voice Authorization unless absolutely needed.

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Merchant

Verification Seal allows your customers to learn more about

your businesses. As a Verified Member, you can proudly

display the Seal on your website or auctions with a redirected

link we provide. Merchant

Verification Seal allows your customers to learn more about

your businesses. As a Verified Member, you can proudly

display the Seal on your website or auctions with a redirected

link we provide.

What it Means to

be Verified?

Included with the Validation Seal,

is 3

Free Search Engine submission. No additional cost, just ensure that the

verification seal is included

on your website for our automated system to begin submitting

your site for indexing.

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Will my DBA name appear on my

customer's statement? Yes. Your DBA name can be any name you do business with and will appear prominently on credit card statements. Of course you should choose a name that matches your marketing material to avoid customer disputes. Some businesses prefer to list their website and phone number as the DBA to reduce charge-backs and to market their brand. Your Legal name is your registered LLC, Corporation, Partnership name or your name, if you are a sole proprietor. We are a home based business (dba). Will my home utility bill qualify as a supporting document? Yes. Make sure your dba (business name) matches the home address and the utility bill is the same home address. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

I have a retail store but I would also like to sell online,

how should I complete the application? You can apply for a Retail Account and then request for an Internet e-Commerce account. Select Retail, pick your choice of a free terminal to save even more. On your application, just write down you would like an Internet gateway added. You will then receive a Internet Addendum rate, which you will fax/email in. Make sure your website includes a terms, privacy statement and refund policy presentable for VISA/MC verification. You will receive 2 statements each month with 2 statement fees, as they are 2 separate accounts. A Retail account and an Internet account are 2 separate accounts, as they carry distinctive different risks identified by VISA/MC/Amex and uses difference technology. A Retail should use a swipe terminal to get the lowest rate and the Internet requires an Internet Gateway Provider such as Authorize.net, where secured data is pass-through with no human intervention. The discount rates and fees will apply accordingly to which account you complete the sale. In both solution, you can of course manually key in entries, which can downgrade your rates. You can review the table rates on the 2 columns above. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Can I use a P.O. Box or UPS address? Required by law, your Doing Business As (DBA) address on file in the USA must be a physical address and not a box. You can however provide a PO Box or UPS address as the alternate Legal Address for your listing when you apply. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Do I need a Manual Imprinter [c5]? Your choice, it is recommended by VISA/MC and is a necessity for Retails with customer facing transactions. A Manual Imprinter is the old fashion plate and swipe you can use to get an imprint. You can also use it on the road or when your terminal goes down. 100% e-commerce merchants with no customer facing, will not need one. Cross it out and initial your name if you do not want it. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Do I still need a bank for deposits or where

will my sales be deposited? Yes, you will need a local bank or U.S. Internet Bank checking account. You can either provide us a signed bank letter with the routing/account number or a photocopy of a voided check that shows your routing/account number/address/security screen lock printed. Normal deposits take about 24-48 hours (next business day) to clear in all banks in the USA. Next day funding available for swipe transactions. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Is Interchange-Plus Rate Plan

available? Yes |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Do I need a Supply Program for paper and ink? Optional. If you don't need it, mark it as N/A - not applicable |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

I cannot decide on which processor bank? United Bank Service, as the name suggest; is a conglomerate of acquiring banks, united and participating in one Looking for testimonials? We do not need to post fictitious or old "testimonials", as we are never short of referrals. The best referrals you can get are merchants who have completed their research recently and have been our client. Get all the referrals you need from our new Merchant listings or cross-verify the seal |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

How long does it to take to get approved and what is the application process? UBS offers same day service. Applications with ALL supporting documents submitted before 12pm Eastern Time, Mondays to Fridays business days, can get approved by 8 pm on the same day. Documents received after 12pm will be processed at midnight and be approved the next business day. You will find more complete details here. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

What are the list of unacceptable merchants

that are considered high risks? All Sexual Oriented or Pornographic Merchant, Gambling, Online Vitamins/Health Supplements and “Get Rich Quick” Books, Programs, Investment, auction etc. Review a copy of our underwriting process under Tier 4 – Unacceptable merchants. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Do you offer special rates for

non-profit 501(c) organizations?

Yes, if you run a shelter-orphanage or provide immunization, food, health or emergency, please visit Non Profit Special Projects. All other non-profit organizations should also provide your 501(c) EIN Tax Letter filing to be categorized as CPS Charity. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Do you offer affiliate or

referral program?

Yes, use the Contact Us form to request for the latest program. Each referral requires you to be in contact with your referee. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Terminal FAQs and Other Statement FAQs We have compiled a list of the most common issues with credit card terminals and standard fees that occur on merchant services. Download a copy for your reference. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Getting Started and Applying Now that you are excited to begin, rest assure you will be pleased with our electronic payment system and financial products. You have to apply online, at the end of the online application, your signature is required. You will be assigned a VISA/MC account number instantly. Apply now and very soon you will begin accepting Visa and MasterCard as well as American Express and Discover Card.

|

.

.UBS an agent of Harbortouch Payments, LLC is a registered ISO/MSP of First National Bank of Omaha